There are more solutions than obstacles. Nicolas Zart

The European Sustainable Transport Investment Plan (STIP) marks a significant step in how the continent tackles its decarbonization of aviation and shipping. It also has direct implications for how Advanced Air Mobility (AAM) as it matures in the region. By targeting both near-term fuel deployment and longer-term revenue certainty, the European Commission is laying financial and regulatory groundwork that AAM stakeholders cannot ignore.

What STIP Does in Practice

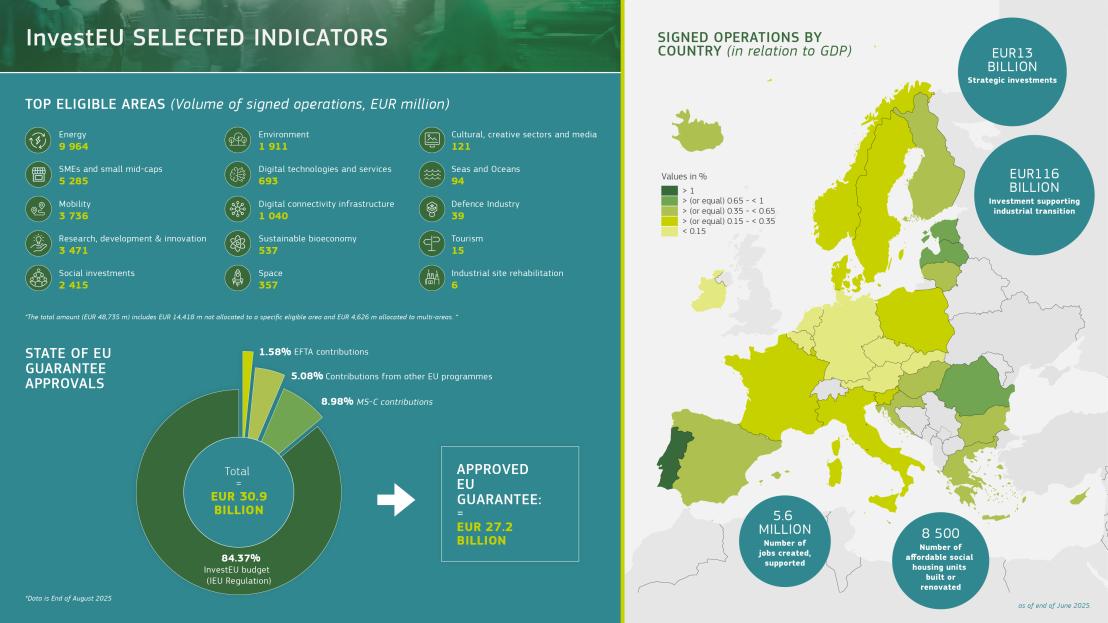

Adopted in November 2025, the Sustainable Transport Investment Plan mobilizes nearly €3 billion (~ $3,5B) to accelerate sustainable aviation fuel (SAF) and sustainable marine fuel production. The timing highlights the problem: second‑generation SAF projects in the EU based on waste and advanced feedstocks, struggles to reach final investment decision, and many planned plants have been delayed or cancelled.

The Plan uses several channels to reduce this investment risk:

- InvestEU will provide guarantees and blended finance for SAF and e‑fuel projects.

- The European Hydrogen Bank is tasked with steering support toward hydrogen‑derived e‑kerosene for aviation.

- A dedicated window in the EU Innovation Fund will co‑fund e‑kerosene projects with high greenhouse‑gas (GHG) reduction potential.

In parallel, a new Early Movers Coalition will pool Member State resources to add about €500 million in targeted support for e‑kerosene, with the aim of giving early projects clear offtake and price signals.

Revenue Certainty, Not Only Capital

The analysis by the International Council on Clean Transportation (ICCT) makes an important point: capital alone will not unlock low‑GHG fuels if producers cannot see stable revenue over time. STIP therefore commits the Commission to design a medium‑term mechanism that links fuel buyers and producers—essentially a structured offtake framework—to de‑risk long‑lead investments.

This aligns with broader EU policy under ReFuelEU Aviation, which creates binding SAF blending mandates for airlines, but STIP complements those mandates with targeted instruments to keep early plants bankable. The combination of regulatory demand and revenue certainty is what investors typically require for multi‑hundred‑million‑euro projects.

Why This Matters for AAM

At ElectricAirMobility.news we have stressed that AAM will scale on infrastructure and energy, not prototypes alone. While most electric AAM platforms in Europe are focused on battery‑electric architectures today (eVTOL, eSTOL, eCTOL), the sector will share airspace, infrastructure, and climate targets with conventional aviation for decades.

Three links to AAM stand out:

- Airport and vertiport ecosystems: SAF and e‑kerosene investments will initially target major hubs, but the same energy and grid upgrades can be planned to support high‑capacity electric charging for eVTOL and eSTOL operations.

- Long‑range AAM concepts: As regional AAM concepts expand beyond pure battery range, hybrid‑electric and hydrogen‑electric aircraft could interface with e‑kerosene or hydrogen supply chains created under STIP.

- System credibility: A European AAM landscape backed by decarbonized conventional aviation improves the overall climate case for new air services, which is critical for public acceptance and political support.

In other words, STIP is not an AAM program on its face, but it shapes the energy and policy environment in which European AAM corridors, vertiports, and power solutions will be built.

Implications for Operators and OEMs

For European airlines, the Plan clarifies that low‑GHG fuels will not be optional at scale; for AAM stakeholders, it clarifies that public funding will increasingly favour solutions integrated into a coherent decarbonization pathway.

For AAM OEMs and infrastructure developers, several practical steps follow:

- Monitor SAF and e‑kerosene projects at future AAM nodes to understand co‑location opportunities for electric charging and hydrogen.

- Align corridor planning with regions where STIP‑backed infrastructure will emerge first, to leverage shared energy investments.

- Engage in emerging producer–buyer platforms, as similar revenue‑certainty mechanisms could be applied to high‑load electric charging or hydrogen for AAM fleets.

This complements themes we have covered around certification, corridors, and capital in 2026: regulatory readiness is necessary, but energy architecture will determine which networks can scale reliably.

A European Signal Beyond 2030

STIP also sends a signal outside Europe. By explicitly linking public funding, hydrogen strategy, and aviation decarbonization, the EU is positioning itself as a reference market for low‑GHG aviation fuels at a time when other regions are still debating their long‑term approach.

For AAM, Europe’s approach reinforces a pattern we see in other strategic documents: decarbonization, digitization, and security are treated as integrated pillars rather than separate domains. As AAM moves from concept to early commercial operations, particularly in European urban and regional settings, the ability to plug into a predictable, low‑carbon energy system will become a competitive advantage.

In that context, STIP is less about a single funding envelope and more about a forward signal: in Europe, aviation’s future—conventional and advanced—will be expected to operate inside a clearly defined climate and investment framework.