By Nicolas Zart | Mobility Futurist & Strategic Intelligence Lead | electricairmobility.news

“There are more solutions than obstacles.” — Nicolas Zart

Spend thirty minutes reading the global Advanced Air Mobility sector in April 2026 and two things become clear. The vehicle layer is closer to commercial reality than it has ever been. And the infrastructure layer that makes those vehicles commercially viable is, in most of the world, not being built.

One analogy cuts through every regional argument, every funding model, every certification timeline. Imagine every car in the world — but no roads, no gas stations, no parking structures. Every boat in the world — but no water, no seaports. Every train with no rails and no stations. Every airplane and helicopter with no airports, no heliports, no control towers.

That is precisely where Advanced Air Mobility stands in 2026. The vehicles are real. The investment is real. The infrastructure that makes those vehicles commercially viable does not yet exist at the scale any business model requires — and is not being funded at the pace any timeline demands.

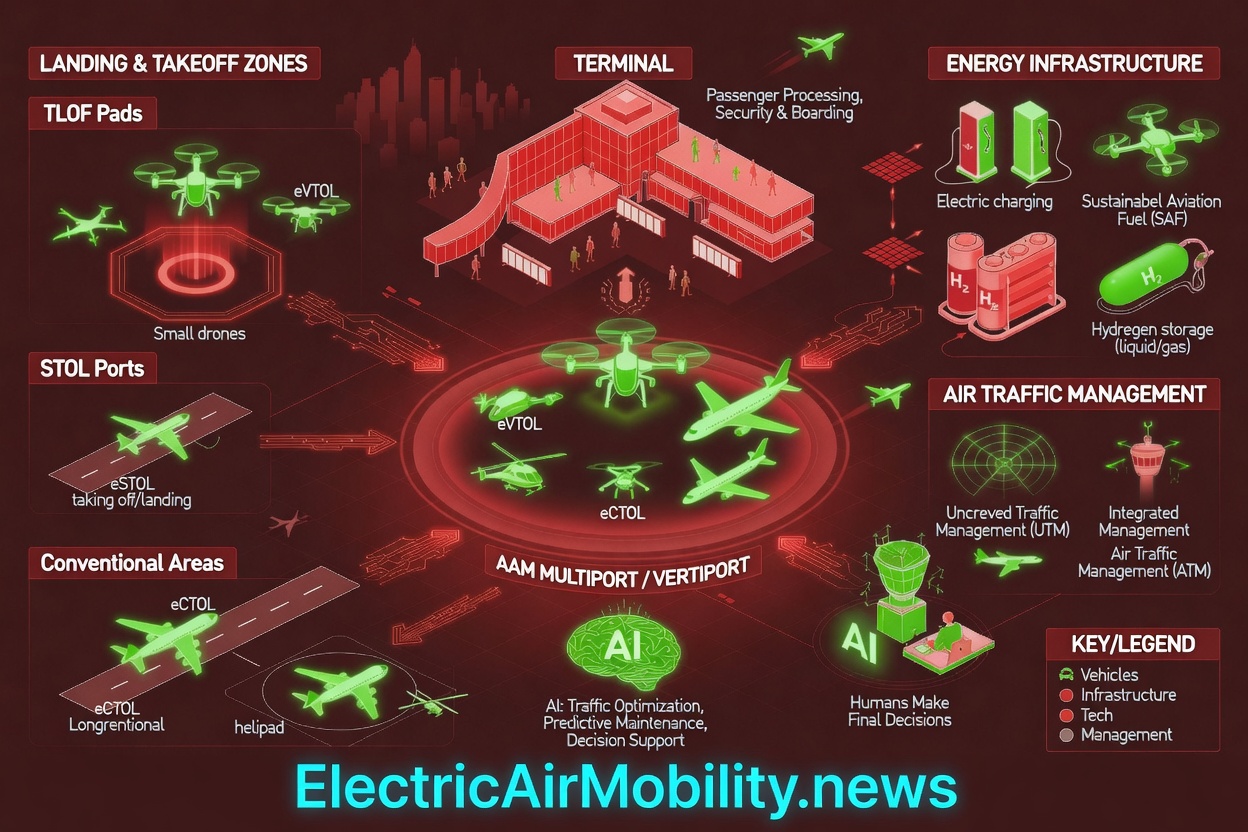

This is not a technical problem. It is a capital allocation problem. Here is a representation.

The Finish Line Is Three Finish Lines

Type certification. Production certification. Operational authorization. All three must be in hand before a single paying passenger boards an eVTOL in U.S. airspace. Press releases routinely describe progress toward the first as though the race is won.

Joby sits at Stage 4 of the FAA’s five-stage type certification process — approximately 80% complete on the company side, 73% on the FAA side as of late February 2026. Archer’s Part 135, 141, and 145 operator certificates certify the airline entity, not the Midnight aircraft. BETA’s “First Certified AAM Technology” is a Part 35 propeller certificate. Industry analysts have pushed commercial eVTOL entry into service back to at least mid-2027.

Flying is not the same as certified to fly. Operations launching is not the same as operations open. The sector that closes that language gap will be the sector that earns lasting investor confidence.

The full credibility framework — with cited press release analysis for all five major OEMs and a question set capital allocators can apply to every future announcement — is available to members.

The Infrastructure Gap Nobody Is Modeling

Twenty-four against 1,504 is not a construction delay. It is a fundamental gap between announced intent and operational reality. And it does not appear in a single major financial model of the sector.

The AAM commercial business model is a dependency chain. OEM viability depends on fleet operators. Fleet operators depend on multiport infrastructure at scale. Multiport infrastructure depends on patient private capital. Patient capital depends on a credible near-term revenue model. Near-term revenue depends on certified aircraft operating commercially. Every layer of this chain is under simultaneous pressure in 2026.

Skyports’ DXV vertiport adjacent to Dubai International Airport reached “technical completion” this month. Four floors. 3,100 square meters. Joby charging infrastructure installed. Rated for 170,000 passengers annually. Waiting for a certified aircraft that has not yet received its type certificate. That facility is the most honest metaphor in AAM right now: built, equipped, and waiting.

When an infrastructure company closes, it doesn’t just remove a balance sheet. It removes the physical operating locations that OEM order books depend on. The order book becomes a commitment to operate aircraft that have nowhere to land.

Five Regions, One Crisis — Expressed Differently Everywhere

The U.S. won the vehicle race. It has not built the road system. Europe built the road and lost the vehicles — Lilium, Volocopter, Rolls-Royce AAM, Airbus CityAirbus NextGen, all gone or paused. The UAE is the only market with sovereign capital aligned to aviation’s time horizon, which is why it’s the only market actually building. China is running a parallel ecosystem under CAAC authority that doesn’t need the FAA and is accumulating operational data while the West debates funding models. Japan is making existing heliport infrastructure work for a compact three-seat aircraft — capital efficient, scale limited.

No single region has all three requirements for AAM commercial success: certified vehicles, patient infrastructure capital, and aligned regulatory frameworks. The sector that solves that three-way coordination problem first will define the next decade.

The sector that emerges from the current consolidation window will not be headquartered in one region. It will be certified in the U.S., operated first in the Gulf, and eventually built on European infrastructure that outlasted its original vehicle assumptions.

The full five-region analysis — with a regional capital allocation scorecard, the distressed European asset opportunity, China’s LAE data implications, and the Japan/SE Asia capital-efficiency thesis — publishes next week and is available in full to members now.

This quick analysis provides sector-level intelligence as of April 2026. It does not constitute investment advice, legal counsel, or due diligence for any specific transaction. This article references active litigation involving AAM OEMs; nothing herein constitutes a legal determination regarding any party. Regulatory references: FAA five-stage type certification process • FAA eIPP program • AFWERX Agility Prime • Part 135/141/145 operator certification framework.

Nicolas Zart is a Mobility Futurist and Strategic Intelligence Lead with 20 years in electric mobility and 14 years covering Advanced Air Mobility from prototype to certification. As founder of ElectricAirMobility.news, he tracks OEM certification timelines, infrastructure capital flows, and regulatory frameworks across North America, the Gulf, and Europe.

electricairmobility.news • linkedin.com/in/nicolaszart • patreon.com/c/TheWaysWeMove